When Should You Apply for an Online MBA?

Timing is everything and prospective students will need to carefully consider how much time is required to apply, and which admissions deadline to pick. Rice Business Associate Dean of Degree Programs, George Andrews, gives his perspective.

Mattress Firm parent considering IPO for chain

"Computers, televisions, washing machines - people are far more willing to buy online. But not so with a mattress, " said Rice Business marketing professor Utpal Dholakia. "They want to lay on a mattress to see how it feels."

The Delta Variant Is Denting Texas’s Construction Industry

Dean Peter Rodriguez weighs in on the impact the pandemic is having on the construction industry. Virus outbreaks could continue to postpone building projects. “Uncertainty,” he said, “is just toxic to growth.”

Admissions Director Q&A: Janice Kennedy of Rice Business’ Jones Graduate School of Business

"I wish candidates understood the breadth and depth of class options available to them at Rice Business once the first year of core courses are completed. Our wide range of learning areas and electives allow students to customize their focus and direction when many other universities don’t. "

Top Feeder Schools To The Consulting Industry

As B-schools begin to release employment reports for the Class of 2021, Poets&Quants takes a last look back at the data from the previous year. Rice Business leads all schools with 62% growth in consulting hires out of its full-time MBA program.

Team-building? Science says pick some moody pessimists too

Conducted as a joint international effort between Rice University, the University of Western Australia, the University of Queensland, and Bond University, this research is among the first to investigate how temperamental diversity influences team creativity and cohesion.

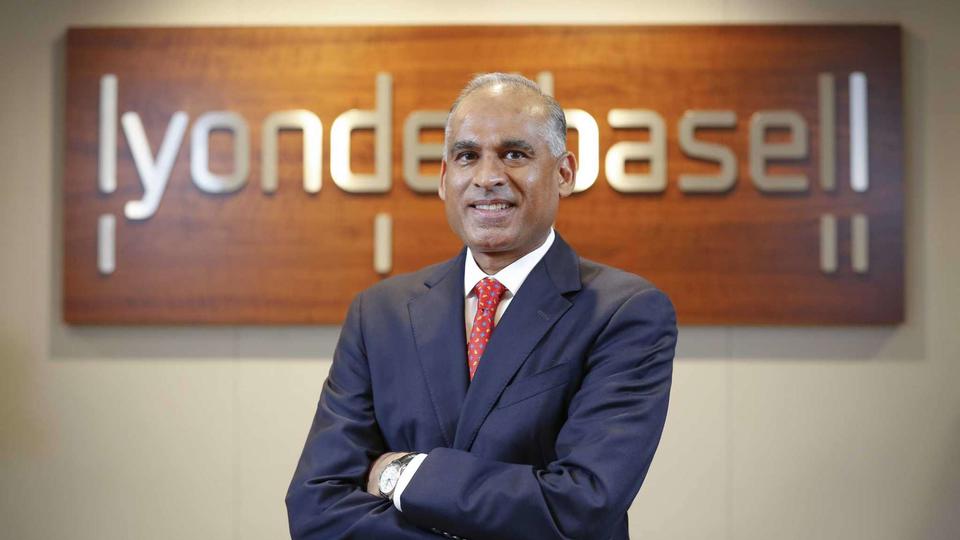

LyondellBasell CEO Bob Patel to retire at end of year

Rice Business professor Yan Zhang says she believes that Patel’s departure is tied to the July 27 chemical leak. "The company has to pick somebody to be responsible. In this situation, making a clear cut between the CEO and the company is a smart move from the company’s perspective.”

Covid Live Updates: Rice University Delays In-Person Classes as Virus Surges

Rice University temporarily turns to online classes as the virus surges across Texas. New York Times updates live.

Giant sculpture of Aztec god makes a big statement about Mexican identity

In Mexico City, a little-known Diego Rivera sculpture honors the partnership of government, art, history -- and science. Rice Business Wisdom editor Claudia Kolker tells the story for National Geographic.

The Best Online MBA Real Estate Programs

The Rice Business Online MBA is ranked by Poets & Quants as the third-best MBA Program for Real Estate. The course offers real estate electives in Capital Markets, as well as in Development and Disruption in Commercial Real Estate.