Image

A new study suggests regions trying to draw venture capital may need to start with commercializable university innovation.

Based on research by Yael V. Hochberg (Rice Business), Daniel C. Fehder (University of Southern California), and Naomi Hausman (The Hebrew University of Jerusalem)

Key takeaways:

For places outside those dominant markets, the question that matters is simple: What makes a place worth investing in?

Many policymakers have tried to solve the problem by bringing in capital directly. They offer tax breaks for early-stage investors, create seed funds or back local venture funds, hoping investment will take root and startups will follow. But new research suggests that this approach may begin one step too late. Venture capital first needs somewhere to go, and something credible to fund.

The harder question is where those credible opportunities come from, and a 2025 study co-authored by Rice Business professor Yael V. Hochberg points to a promising answer: publicly funded university research.

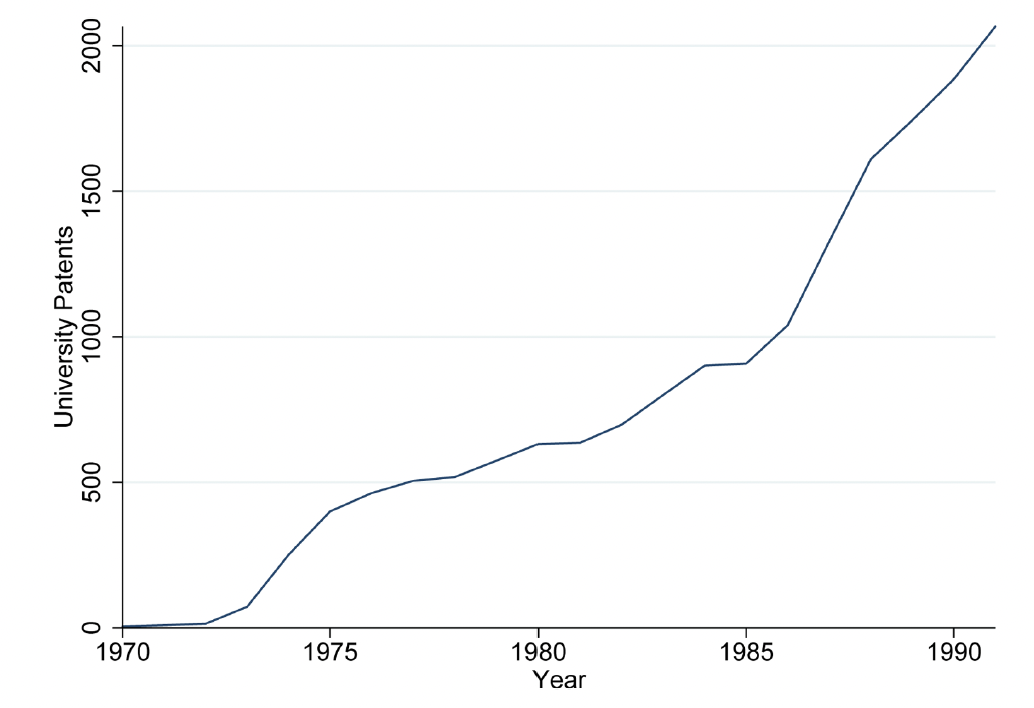

Published in the Journal of Financial Economics, the study examines the major policy shift created by the Bayh-Dole Act of 1980, which gave universities stronger incentives to patent and license discoveries from federally funded research. The law gave Hochberg and her colleagues a way to study whether venture capital follows the supply of university innovation it can help bring to market.

Before the Patent and Trademark Law Amendments Act (1980), sponsored by U.S. Sens. Birch Bayh and Bob Dole, many federally funded university discoveries faced a chokepoint on commercialization. Inventions and related intellectual property from that research were typically assigned to the federal government, and much of it was never patented or marketed. Universities could produce boundary-breaking research, but the incentives and infrastructure for moving those discoveries into industry were weaker.

The law changed those incentives. Allowing universities to hold property rights to federally funded discoveries encouraged more patenting, licensing and technology transfer. It wasn’t that university research suddenly become more valuable, but industry and investors were more easily able to see and assess it.

“Venture capital is often treated as the scarce ingredient in a startup ecosystem,” Hochberg says. “But investors need credible opportunities — meaning, research that has moved far enough from the lab to be evaluated, funded and developed. Without that, adding venture capital funds does very little.”

Around this same time as the new law, regulation changes increased how much money VC firms had available. The timing of all this gave Hochberg and her co-authors a useful way to test where private capital flowed once more university research could move toward commercial use.

Regions that develop the research base, technology transfer infrastructure and local capacity to turn discoveries into investable opportunities will naturally see venture investment capital flow to them.

The key insight of Hochberg’s study lies in the pattern of movement. After Bayh-Dole, venture capital flowed toward the regions around universities, especially into industries connected to the preexisting research strengths of those universities.

To test that pattern, Hochberg and her co-authors compared industries within the same local area. Consider the contrast they use between the University of Texas at Austin and Johns Hopkins University. Before Bayh-Dole, UT Austin had a strong electrical and computer engineering department, while Johns Hopkins was especially strong in biosciences. If university innovation helped attract venture capital, the researchers expected to see different patterns in each region: in Austin, more VC flowing into electronics and computer-related industries; in Baltimore, into pharmaceutical and bioscience.

And indeed, that’s what they found. The average university county saw a $23.4 million increase in VC funding over the 20 years surrounding Bayh-Dole and related regulatory changes. The post-1980 increase in venture capital was strongest in the local industries most closely tied to each university’s research strengths. That pattern held even after the researchers accounted for broader industry trends and preexisting distributions of venture capital.

The study clarifies a chicken-or-egg conundrum: whether innovation attracts capital, or capital creates innovation. By using Bayh-Dole as a policy shock, Hochberg’s work shows that an increase in commercializable university innovation helped draw research-relevant funding into nearby regions.

“Capital is important,” Hochberg says, “but capital without something to fund doesn’t help create entrepreneurial ecosystems. Regions that develop the research base, technology transfer infrastructure and local capacity to turn discoveries into investable opportunities will naturally see venture investment capital flow to them.”

The study focuses on a specific historical shift, and venture capital is only one pathway from university research to economic activity. So, future research could examine how other forms of capital, other policy settings or non-VC commercialization channels shape the same process.

Still, the central lesson holds: Private funding follows innovation — and public research can help create it.

Written by Scott Pett

“Innovation and Capital,” Journal of Financial Economics (2025).